- Главная

- Разное

- Дизайн

- Бизнес и предпринимательство

- Аналитика

- Образование

- Развлечения

- Красота и здоровье

- Финансы

- Государство

- Путешествия

- Спорт

- Недвижимость

- Армия

- Графика

- Культурология

- Еда и кулинария

- Лингвистика

- Английский язык

- Астрономия

- Алгебра

- Биология

- География

- Детские презентации

- Информатика

- История

- Литература

- Маркетинг

- Математика

- Медицина

- Менеджмент

- Музыка

- МХК

- Немецкий язык

- ОБЖ

- Обществознание

- Окружающий мир

- Педагогика

- Русский язык

- Технология

- Физика

- Философия

- Химия

- Шаблоны, картинки для презентаций

- Экология

- Экономика

- Юриспруденция

Introduction to economics. Demand & supply презентация

Содержание

- 1. Introduction to economics. Demand & supply

- 2. The Control of Prices At the equilibrium

- 4. Minimum price A price floor set by

- 5. Maximum Price A price ceiling set by

- 6. Setting a minimum (high) price To protect

- 7. How do Gnvts deal with Surpluses associated

- 8. Setting a Maximum (low) price Fairness, famine,

- 9. Underground Markets Traditionally referred to as black

- 10. Activities Listen to the podcast http://www.bbc.co.uk/programmes/b06yn9zv

Слайд 2The Control of Prices

At the equilibrium price there will be no

shortage or surplus.

May not be the most desired price - Government intervention

Government sets a minimum price above the equilibrium there will be a surplus

Government sets a maximum price below the equilibrium there will be a shortage

May not be the most desired price - Government intervention

Government sets a minimum price above the equilibrium there will be a surplus

Government sets a maximum price below the equilibrium there will be a shortage

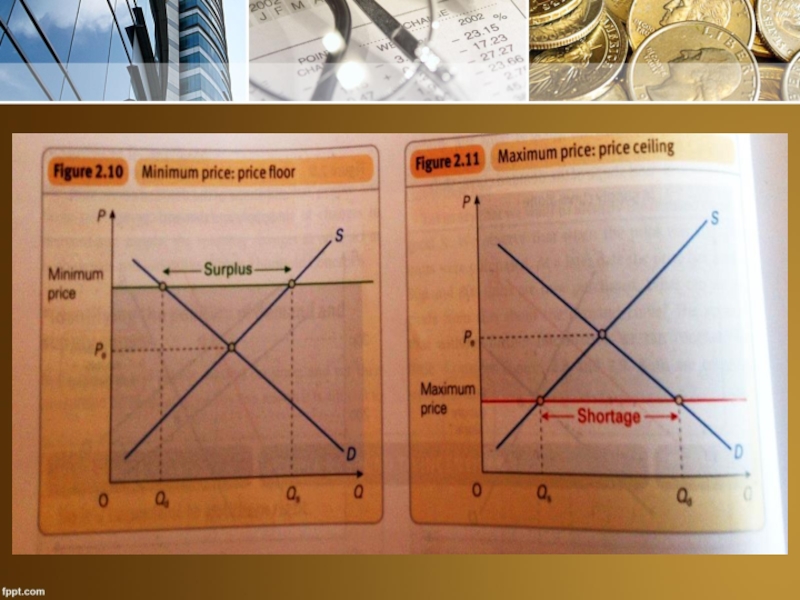

Слайд 4Minimum price

A price floor set by government or some other agency

The

price is not allowed to fall below this level (although it is allowed to rise above it)

Слайд 5Maximum Price

A price ceiling set by the government or some other

agency.

The price is not allowed to rise above this level (although it is allowed to fall below it)

The price is not allowed to rise above this level (although it is allowed to fall below it)

Слайд 6Setting a minimum (high) price

To protect producers incomes (industries subject to

fluctuations)

To create a surplus ( to be stored for future shortages)

In the case of wages to prevent workers wages falling below a certain level (gnvt policy on poverty and inequality)

To create a surplus ( to be stored for future shortages)

In the case of wages to prevent workers wages falling below a certain level (gnvt policy on poverty and inequality)

priceTo protect producers incomes (industries subject to fluctuations)To create a surplus")

Слайд 7How do Gnvts deal with Surpluses associated with minimum prices?

Buy &

store, destroy, sell abroad

Artificially reduce supply by restricting producers – introducing quotas

Raise demand - ^ advertising, alternative uses - impose taxes or subsidies on substitutes

Problems – evasion, inefficiency

Artificially reduce supply by restricting producers – introducing quotas

Raise demand - ^ advertising, alternative uses - impose taxes or subsidies on substitutes

Problems – evasion, inefficiency

Слайд 8Setting a Maximum (low) price

Fairness, famine, war

Associated problems “first come first

served”

Preference to regular customers

May lead to underground markets – ignoring price and selling illegally

Rationing – gnvt restricts amount people allowed to buy

Preference to regular customers

May lead to underground markets – ignoring price and selling illegally

Rationing – gnvt restricts amount people allowed to buy

priceFairness, famine, warAssociated problems “first come first served” Preference to regular")

Слайд 9Underground Markets

Traditionally referred to as black markets

Government prices and controls are

ignored and people illegally sell at whatever price illegal demand and supply create

Слайд 10Activities

Listen to the podcast http://www.bbc.co.uk/programmes/b06yn9zv

Read the article and answer the

questions

http://pearsonblog.campaignserver.co.uk/?p=19578

http://pearsonblog.campaignserver.co.uk/?p=19578